The entire carbon credit system is fraught with volatilities. Adding fuel to the fire has been a recent development wherein the Zimbabwean government declared that it would claim half the revenue generated from offset projects developed in the country. All past agreements thus stand null and void [1]. It should also be noted that this news comes in the wake of the media report that surfaced during the first quarter of the year about the Kariba project in Zimbabwe, which alleged that the emissions avoided were vastly overestimated [2]. For the first time, a country from the global south is challenging an arrangement where companies in the global north are being benefitted. Although Zimbabwe has a legacy of making quick and controversial policy decisions, the country may after all have a point this time. Last year, Gabon also questioned the right of foreign companies to set up offset venture in the country without first going through the government [3].

While this is happening in the international market, I can think of a couple of challenges from the domestic side. While there are a handful of companies claiming carbon neutral through offsets, several Indian firms are warming up to this idea of carbon credits in the journey to emerge carbon neutral and Net-Zero. While regulations are getting tightened around the world even on the use of these terms [4], I felt it is time to pose basic questions on some of the practices that are observed in India. I thought of writing about this in the wake of the RBI considering diverting CSR funds towards climate change [5].

Some of the early movers among the Indian companies have been supporting NGOs by funding projects which generate carbon credits for these to be used later to offset their emissions. So, where does the challenge lie? The challenge is in the funding that is coming from the CSR fund pool and carbon credits secured in return.

For readers who do not understand Indian CSR, here is a quick brief on the same: In India under the Companies Act of 2013, the section 135 requires a company to spend at least two percent of its average net profit generated during the three preceding financial years in pursuance of the Corporate Social Responsibility (CSR) policy [6]. There are a set of rules that support this section, which are known as the CSR Rules [7]. We shall consider a couple of requirements from the said rules to evaluate whether the Carbon Credits secured by these companies through CSR funds will qualify within the criteria or not.

- CSR shall not include activities undertaken in pursuance of normal course of business of the company.

Aligning to the best practices and responding to consumer and customer requirements are normal course of business. There are enough business drivers within a business to consider carbon offsets. When a company makes a commitment to be Net-Zero, the ESG ratings accommodate that, investors and clients in turn considers that. While it is not a legal requirement, but it turns to be an obligation of the business. Hence, the first challenge will be for companies to establish that it is not a normal course of business.

2. Any surplus arising from the CSR activities shall not form part of the business profit of a company and shall be ploughed back into the same project or shall be transferred to the unspent CSR account ………….

In the subsequent FAQ [8], surplus is defined as income that is generated from the spend on CSR activities, e.g., interest income earned by the implementing agency on funds provided under CSR, revenue received from the CSR projects, disposal/sale of materials used in CSR projects, and other similar income sources. The surplus arising out of CSR activities shall be utilised for CSR purposes only.

These credits acquired by the company have a market value. A good quality credit currently has a value between $5 to $10 [9] and is expected to increase in the coming years. Although the company is not earning revenue in cash, this is an expense saved for the company, if it is securing these credits in lieu of the CSR expenditure incurred on the project. The second challenge is to treat the value of the carbon credits.

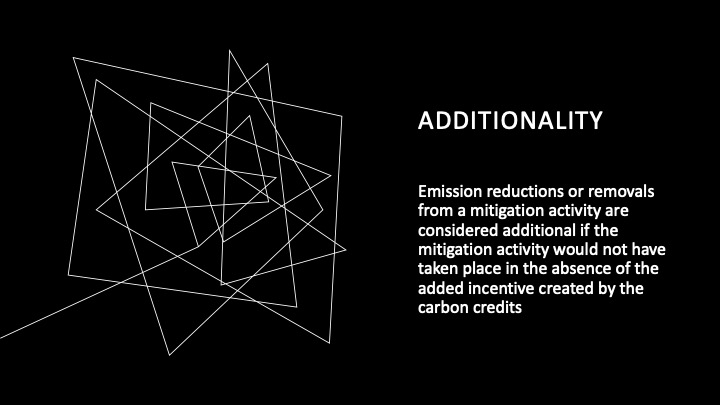

There is one more dimension that must be checked from the original Project Design Document (PDD), which was subject to validation and verification before issuance of credits. Any project undertaken should showcase among other things that the project is “additional” [10]. In the context of crediting mechanisms, emission reductions or removals from a mitigation activity are considered additional if the mitigation activity would not have taken place in the absence of the added incentive created by the carbon credits [11]. This means that the revenue from the credits should go back to the project to ensure that the project is sustainable. So, what happens when the project funder acquires the credits free of cost? This poses a foundational question on the project additionality.

It can be argued that the project will not attract funding because of low or even negative IRR and hence to attract CSR funds, carbon credits can be an incentive. That is a good additionality argument. But even in that case the surplus clause will kick in because through the investment the company is acquiring a commodity which has a market value.

While the global clamour on carbon credit has hit a new high in the midst of the regulation clampdown on greenwashing, it will be a good opportunity to bring clarity during these early days in India. Action on carbon offset by corporates has just begun and it might be helpful for the Ministry of Corporate Affairs (MCA) to bring clarity on CSR funding to acquire carbon credits. It should be kept in mind that many of these projects will not happen if they were not funded by CSR because of the cost of capital. In the meantime, it must be seen that the revenue from the carbon credits ensures the sustainability of the project.

[1]

[2]

[3]

[4]

https://www.corporateknights.com/leadership/carbon-neutral-net-zero-global-greenwash-crackdown/

[5]

[6]

https://www.mca.gov.in/content/dam/mca/pdf/CompaniesAct2013.pdf

[7] https://www.mca.gov.in/bin/dms/getdocument?mds=80v%252FwnuSUTjujZt5EVX2fA%253D%253D&type=open

[8]

https://www.mca.gov.in/Ministry/pdf/FAQ_CSR.pdf

[9]

[10]

https://www.offsetguide.org/wp-content/uploads/2020/03/Carbon-Offset-Guide_3122020.pdf

[11] https://www.edf.org/sites/default/files/documents/what_makes_a_high_quality_carbon_credit.pdf

Fantastic Article!Looking forward for some more read throughs!